On July 31, 2023, The European Commission (EC) made a significant stride toward fulfilling the goals of the European Green Deal by officially embracing the European Sustainability Reporting Standards (ESRS). These standards define the mandatory sustainability data that companies participating in the Corporate Sustainability Reporting Directive (CSRD) must disclose and provide clear guidance on the reporting methodologies.

Before we take a closer look at who will be impacted by these CSRD reporting standards, let’s look at a timeline for how we arrived here in the first place.

2014 – The European Commission adopts Directive 2014/95/EU. This Non-Financial Reporting Directive (NFRD) requires qualifying companies to include in their annual reports, or separate filings, and non-financial statements their impact on a number of environmental, social and governance (ESG) issues, including treatment of employees, diversity on company boards, respect for human rights, environmental protection and social responsibility.

2019 – The European Commission endorses the Green Deal, an ambitious strategy to transition Europe to a circular economy to reduce waste and pollution and reach carbon neutrality by 2050. Fostering sustainable economic growth is considered a critical element of the Green Deal’s success, so emphasis is placed on funding economic activities supporting ESG activities. To identify companies that are actively supporting ESG activities, the EC also shares its intention to review the NFRD.

2020 – The EU Taxonomy Regulation comes into effect to address greenwashing. Taxonomy is a complex science-based classification system for identifying activities that can be considered environmentally sustainable. The European Union (EU) Taxonomy’s definitions and rules enable market participants to identify and invest in sustainable assets with more confidence.

2022 – The European Commission adopts the Corporate Sustainability Reporting Directive (CSRD), which will replace and improve upon the NFRD. Not only does the CSRD mandate more detailed reporting by establishing a double materiality threshold which applies to both financial and impact materiality, but it also applies to more companies. The European Financial Reporting Advisory Group (EFRAG) is tasked with identifying the specific reporting standards needed. Emphasis is placed on developing a set of standards that align with various global standards already in place. The CSRD also includes references to the EU Taxonomy.

2023 – After receiving recommendations from EGRAG EFRAG and hearing public comments, the European Commission issues the European Sustainability Reporting Standards (ESRS). Companies falling under CSRD now have specific disclosure reporting guidelines.

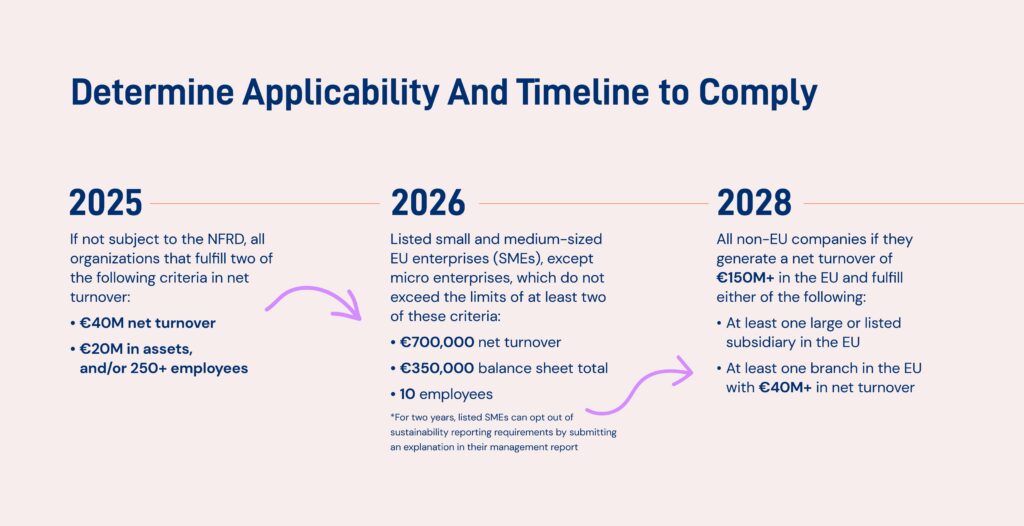

2025 – On February 26, the EU proposed an Omnibus package of regulatory changes, which includes adjustments to the CSRD framework aimed at “easing” compliance burdens. Key proposals include extending reporting deadlines for certain companies, simplifying disclosure requirements and providing more flexibility in how sustainability data is reported. Regardless of the outcome of the proposal, organizations should still be prepared to report on sustainability requirements.

While the NFRD affected approximately 12,000 companies, almost 50,000 companies (75 percent of businesses in European Economic Area) fall under the criteria for CSRD.

The CSRD initially applied to large public-interest EU companies with over 500 employees, but over several years expands to eventually include small, medium and large companies meeting certain financial thresholds. 2024 reporting requiring all organizations already within the scope of the NFRD has passed.

CSRD reporting obligations begin in 2025 for large, public-interest companies in the EU with 250 or more employees and a balance sheet total exceeding €20 million or net turnover exceeding €40 million. As mentioned above, the proposed Omnibus package may affect these reporting requirements, and organizations are encouraged to see how the proposed changes may affect them.

Before looking at the disclosure standards outlined in ESRS, it is important to consider the “why” behind the required disclosures. The EC wants stakeholders to clearly understand impacts, risks and opportunities a company is facing as it relates to ESG issues. This includes both the potential negative and positive impacts an organization has on the community and environment, as well as any sustainability related risks and opportunities faced by the organization.

To make an honest, informed assessment, this requires information related to a company’s governance structure, its internal control and risk management system, as well as its strategy and approach to ESG issues, including policies, procedures, processes, and performance.

If all companies are required to disclose the same information, only then will stakeholders be able to identify those companies that are truly making meaningful and measurable inroads toward the European Green Deal.

ESRS 1 addresses the mandatory concepts and principles to be followed by companies when preparing sustainability statements under the CSRD.

ESRS 2 addresses specific disclosures related to companies’ general business, as well as their compliance and governance strategy. Additionally, their impact on ESG and the risks and opportunities faced under ESG (often referred to double materiality) are required.

Environment: E1-E5 covers disclosures related to the environment (climate change, pollution, water and marine resources, biodiversity and ecosystems, resource use and circular economy).

Social: S1-S4 covers disclosures related to social standards (employees, workers in value change, affected communities and consumers).

Governance: G1 covers disclosures related to the ethics of a company in regard to their corporate practices.

While the ESRS can feel intimidating at first glance, companies with a robust automated process in environmental, health, safety and sustainability in place will be able to leverage their expertise to comply with ESRS requirements more efficiently.

By following the below steps, you can help prepare your company for CSRD reporting:

For more information on how our regulatory compliance software can help you navigate CSRD requirements, check out our solutions page below!

Share